Every day, governments, financial institutions and corporations have a choice to make: invest in physical assets that emit greenhouse gases and harm nature or prioritize the development of green solutions that foster a stable, resilient and equitable economy. As communities face the harsh impacts of climate change, the choice to build a sustainable future is becoming clearer.

Estimates suggest around $5 trillion of capital will be needed every year by 2050 to meet climate and biodiversity goals. These investments are essential to research and scale new low-carbon technologies, to substitute the existing capital stock with sustainable alternatives, to shift business models away from harmful practices and to enable rich countries to support vulnerable ones in their climate resilience and biodiversity protection, all while ensuring that historically marginalized communities share in the broad prosperity created.

Systems Change Lab is tracking six major shifts in the finance sector that can drastically transform how investments are scaled and allocated for a sustainable future. If these transformations are achieved together, it will enable the fundamental changes needed for the planet and people to thrive:

1) Measure, Disclose and Manage Climate- and Nature-related Financial Risks

The transition to a decarbonized and nature-positive future will disrupt products and services, especially those that have high emission outputs and are harmful to ecosystems. Not only are there risks to physical facilities, including factories and operations, but also to existing business models.

Corporations, financial institutions and regulators must have access to information and a clear understanding of the risks and opportunities to target investments that advance sustainable transformations of their businesses.

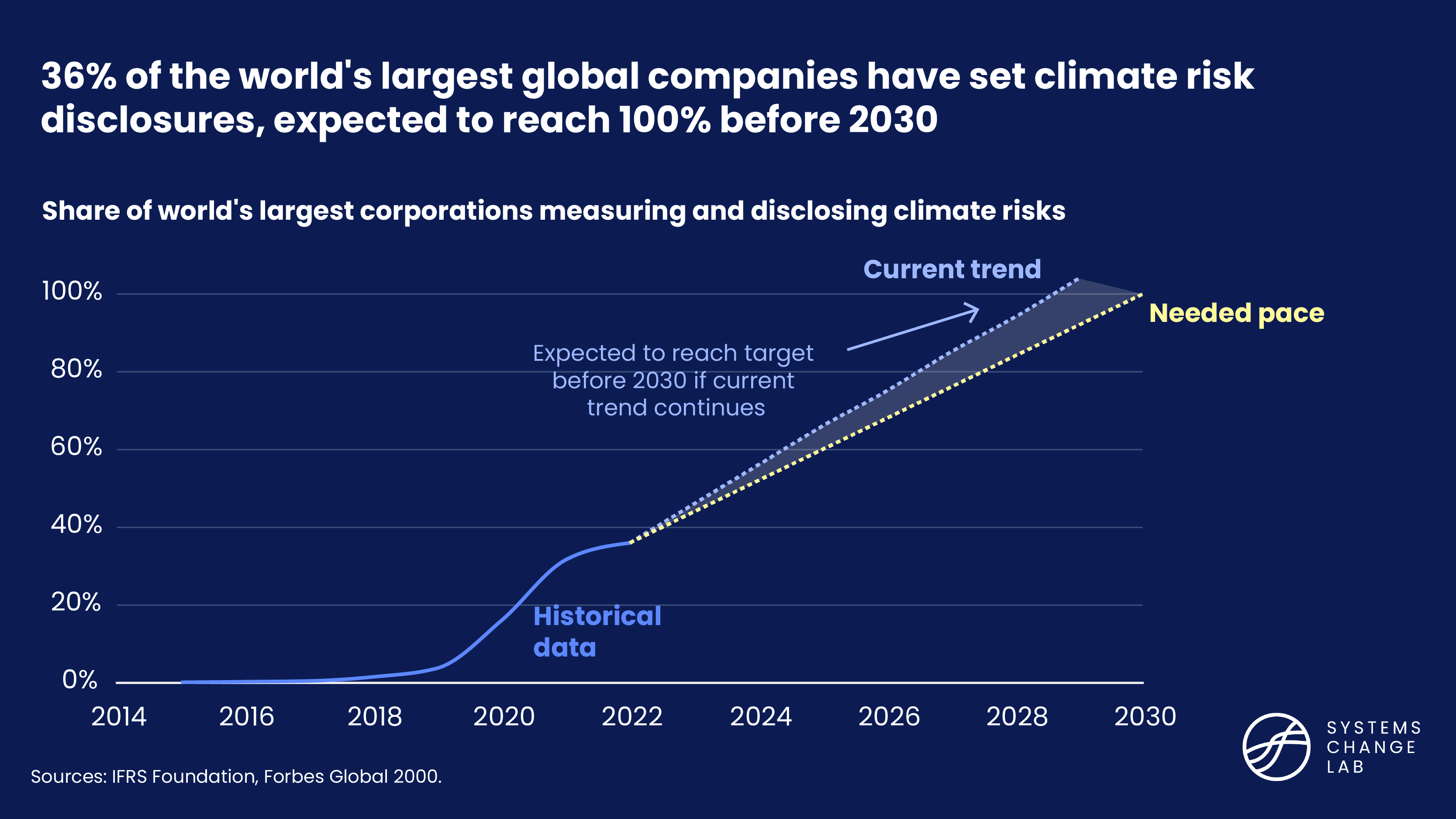

Accurate disclosures are needed to allow financial institutions and governments to deploy capital efficiently and monitor and manage risks at a portfolio and systemic level. An increasing number of corporations disclose their climate risks under standards created by the Sustainability Accounting Standards Board, which follows recommendations from the Taskforce for Climate-related Financial Disclosures. Analysis from the Systems Change Lab shows that 36% of the largest global companies have set climate risk disclosures (up from about 32% in 2021). By 2030, all of these businesses need to provide disclosures.

There is also positive momentum regarding nature-related disclosures. The Taskforce for Nature-related Financial Disclosures framework is in the process of being finalized and has also received substantial support from the private sector.

Despite progress in adoption, disclosures have been on a voluntary basis with inconsistent quality and gaps in coverage. Governments must play a crucial role in mandating high-quality disclosures to ensure there is universal coverage and uniformity in reporting. Regulators are stepping up. The world’s largest economies and capital markets are considering mandating such disclosures and incorporating them into the supervision of their economies.

In 2022, 36 countries planned or set mandatory climate-related disclosures aligned with the Taskforce for Climate-related Financial Disclosures. The countries include Brazil, India, Japan, the United Kingdom, countries in the European Union and the United States.

2) Scale Up Public Finance for Climate and Nature

The public sector can play a significant role in the protection of climate and nature by investing directly in climate initiatives and steering private markets, all while formulating policies that promote an equitable transition toward a green economy.

Governments are the biggest allocators of capital in most economies, and their investment is crucial in areas where private finance is unable or unwilling to take a leading role such as development of new, high-risk technologies, public infrastructure and supporting underserved and marginalized communities.

Recent climate legislation such as the U.S. Inflation Reduction Act is a concrete example of how the public sector can steer markets in new directions that favor decarbonization, allocate public finance to invest and develop new low-carbon solutions, and address inequities in disadvantaged communities.

For example, policies like the Inflation Reduction Act are expected to significantly grow the amount of government investments in research and development of low-carbon technologies, currently estimated to be around $24 billion per year globally. Reactions from the business community, especially the finance sector, have been positive, recognizing that the legislation is expected to dramatically increase the scale of business opportunities and investments in both mature and nascent climate solutions.

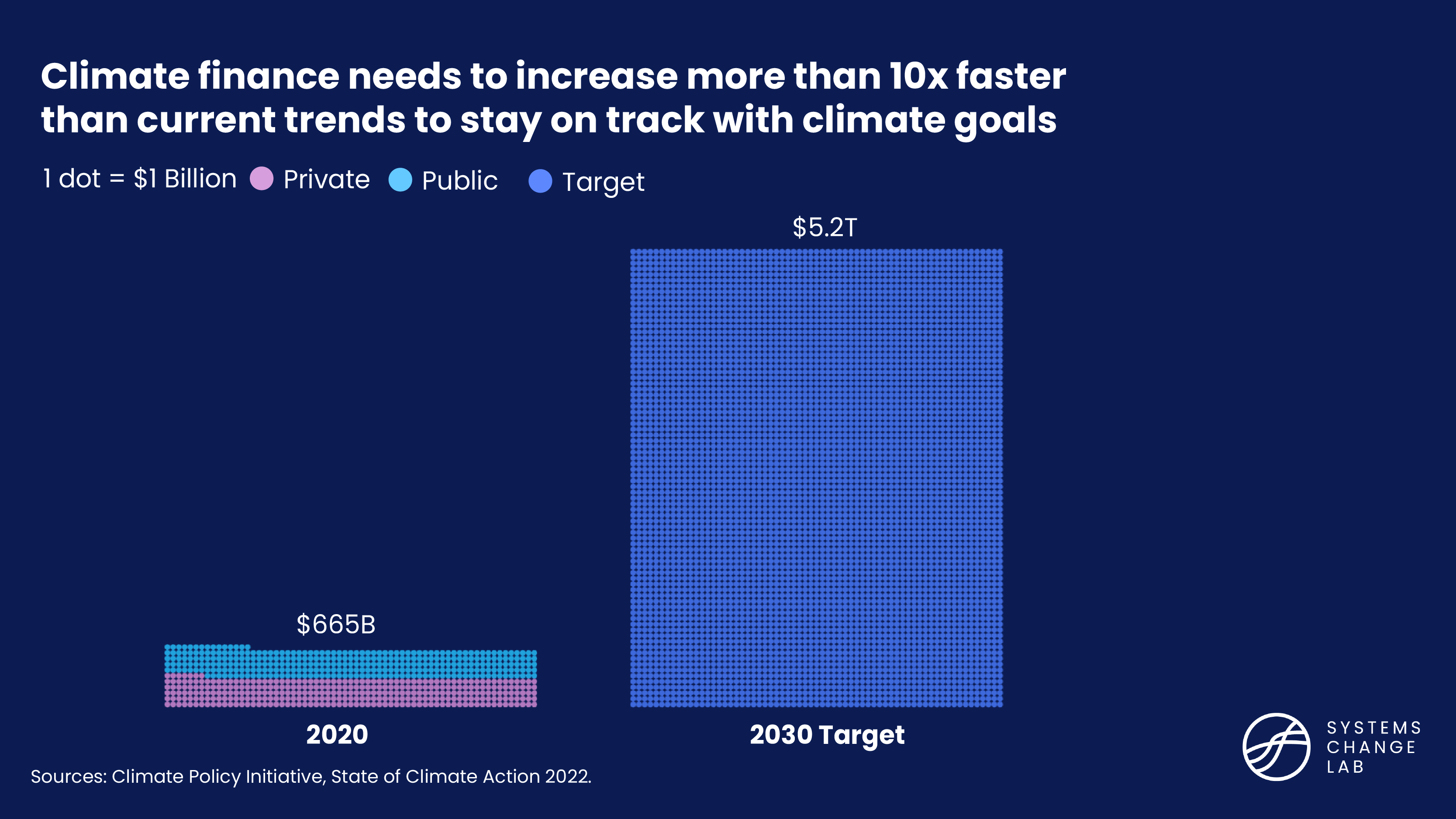

To prevent some of the worst impacts of climate change, estimates suggest that public climate finance of at least $1.3 trillion will be needed every year by 2030. In 2020, it totaled $333 billion, significantly below the levels required to meet that target. To bridge the gap, financing needs to grow by more than eight times the historical rate.

Fortunately, the Inflation Reduction Act and similar climate-focused legislation being planned in Europe and other major economies will help. Some estimates suggest that the Inflation Reduction Act will result in $1.2 trillion over 10 years in public incentives on clean technologies, with potential to go further depending on uptake.

Finally, public finance from developed countries can play a key role in meeting their annual $100 billion commitment to support developing countries on climate mitigation and adaptation. In 2020, the amount totaled $83 billion, falling short of the target.

The quality of financing also needs to improve as multilateral development banks, one of the main providers of climate finance, can increase share of grants and concessional loans to give developing countries greater financial flexibility in addressing their climate needs. New initiatives such as the Bridgetown Initiative that aim to help developing countries meet their climate goals by reforming the global financial architecture are gaining momentum and garnering attention.

3) Scale Up Private Finance for Climate and Nature

Meeting climate and nature goals also depends on the participation of the private sector. Some projections suggest that three-quarters of the estimated $5 trillion needed per year by 2030 will come from private sources while historically there has been an even split between public and private climate finance. The corporate sector can help scale the climate solutions needed to decarbonize our economies, but investments need to accelerate more than 10 times to reach the estimated $2.6 trillion to $3.9 trillion per year from the private sector by 2030.

There are some signs of progress. Innovative firms have identified which new risks and business opportunities are developing out of the economic transition. An increasing number of firms are adapting their strategies and business models to reduce their exposure to such risks, setting net-zero targets to cut their emissions and investing in new products and services to grow in this new economic reality.

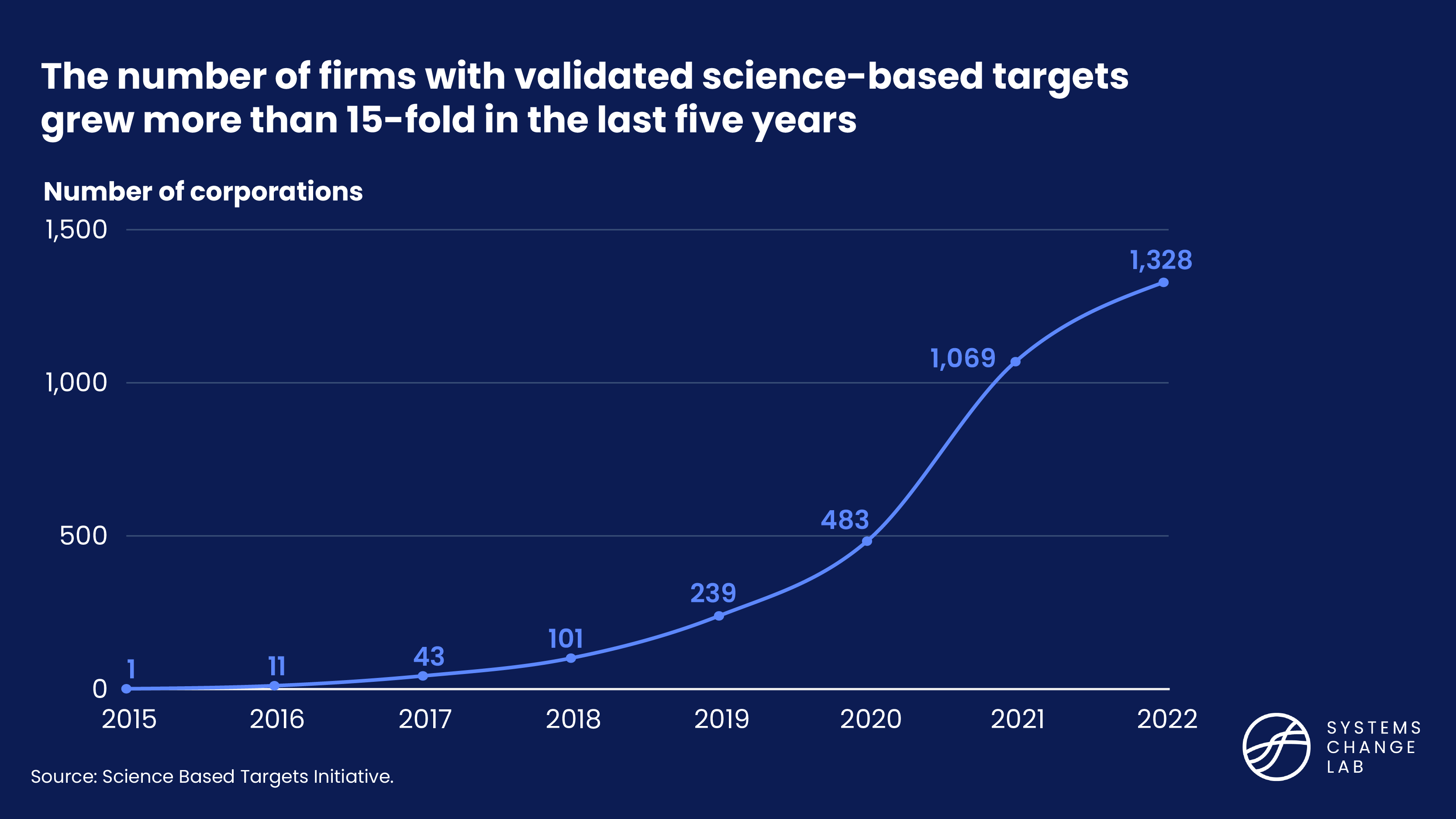

The number of corporations with science-based targets that have been independently validated by the Science Based Targets initiative to align with the goals of the Paris Agreement grew 20% in 2022 and continues to increase. Such emissions-reduction targets are expected to influence their business strategies and investments, both on their own operations as well as capital allocated to other firms. But such corporate targets will require further scrutiny, improvement, robust oversight and implementation monitoring.

Investors are also aligning their investment allocation — about $7.5 trillion in assets — to net-zero targets by pushing high-emitting companies to change their businesses and shifting capital toward firms developing low-carbon solutions.

Investor initiatives like Climate Action 100+ have engaged with the largest corporate emitters of greenhouse gases via joint shareholder proposals and escalation actions to reduce their emissions and adapt their businesses. The pool of capital aligned with net-zero targets is expected to expand as investors increasingly realize that sustainable business practices not only result in more competitive and resilient firms but also align with profitable financial returns.

Finally, getting private finance involved in supporting developing countries in their decarbonization and adaptation efforts has long been a goal. While the record of de-risking private finance is mixed, recent initiatives like the Energy Transition Accelerator and the Just Energy Transition Partnerships are novel attempts to harness private finance to decarbonize middle- and low-income countries.

4) Extend Economic and Financial Inclusion to Underserved and Marginalized Groups

Our current economic and financial systems have failed to be inclusive in sharing economic prosperity, resulting in historical inequities that have been perpetuated and sometimes worsened, further marginalizing already underserved groups.

The transition to a decarbonized and sustainable economy provides an opportunity for historically underserved communities to share in new prosperity which will contribute to a more inclusive, fair and democratic society.

Success in implementing a just transition will enable the world to meet the UN Sustainable Development Goals of eradicating poverty, reducing inequality and promoting full employment. Such progress is not only morally right but will also gain popular support and provide the political legitimacy and social stability that allow the transition to be accomplished.

To do this, governments can coordinate with the private sector to create high-quality employment in green industries that will enable communities to work and participate in building a decarbonized future. Additionally, access to well-regulated financial resources, such as bank accounts and well-regulated lending, can help them build the financial security needed to become resilient and adapt to a changing environment. In 2021, 76% of the world's adult population had access to a bank account, indicating that the remaining 1.4 billion adults were still considered “unbanked.”

The public sector can establish the infrastructure that facilitates access to financial services for all while also providing direct assistance to vulnerable communities with cash transfers, which serve as an entry point into the formal financial system and are an important aspect of social safety nets.

5) Price Greenhouse Gas Emissions and Other Environmental Externalities

One of the largest challenges to shifting investments to a more sustainable future is the lack of accounting for the negative external costs generated by the fossil-fuel industry and other high polluters that get passed into society. These indirect costs, often referred to as “externalities,” are not adequately captured by prices despite the negative effects attributed to them such as lower quality of life, economic disruption and environmental degradation. As a result, polluters profit from their harmful activities and are not held accountable for these externalities while distorted prices can discourage changes in consumption patterns and efforts to reduce pollution.

Applying a direct carbon price via carbon markets or a carbon tax on polluters can ensure that these external costs are properly accounted for in planning and decision-making that reduces environmental harm. While carbon pricing is not a silver bullet to solve climate change, it can complement a broader toolkit of approaches such as industrial policy and incentives for research and development of new low-carbon technologies. Similarly, taxing other environmentally harmful activities such as air pollution, natural resource use and waste can internalize their externalities which are estimated to reach $7.8 trillion annually by 2050.

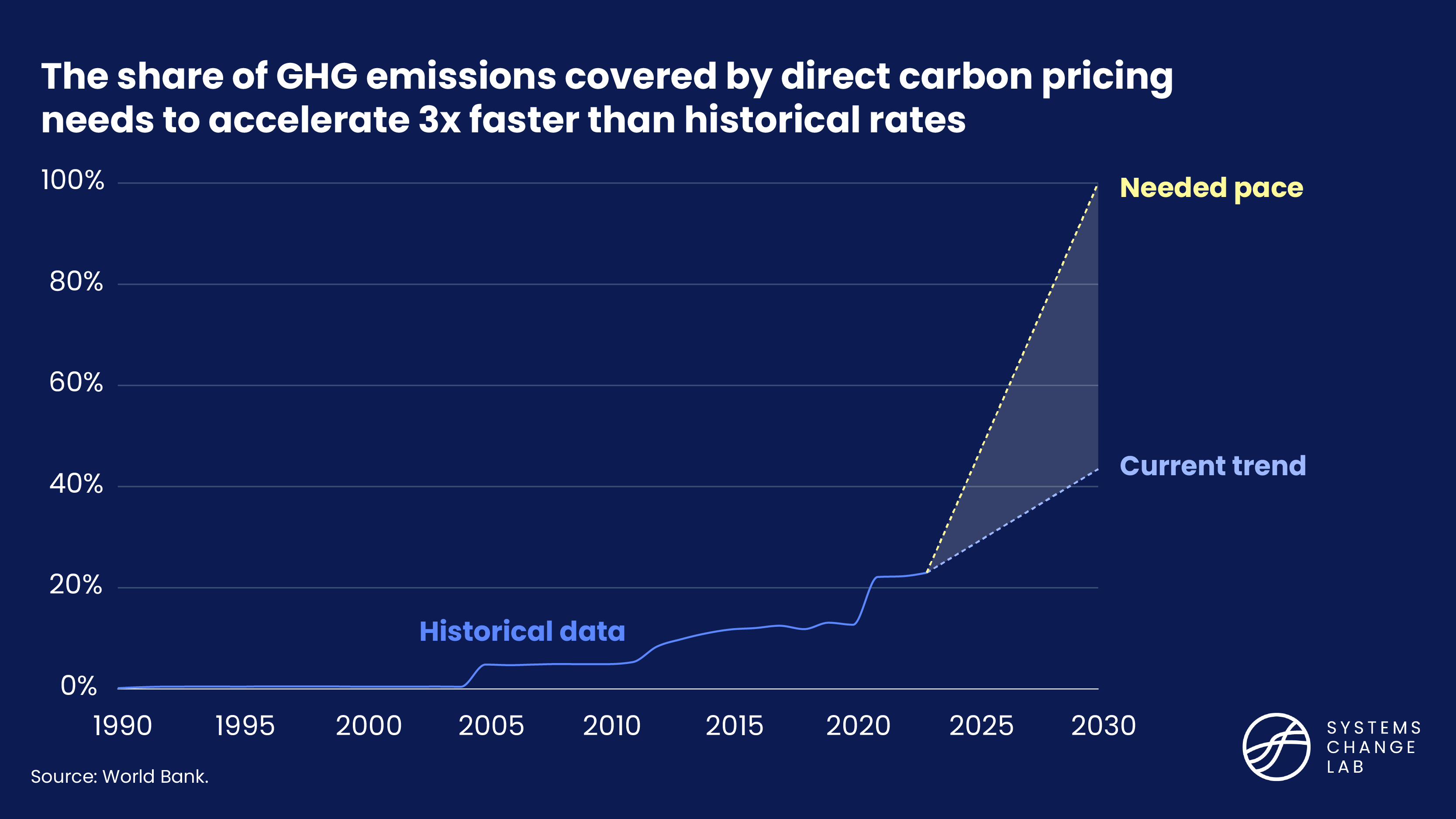

Currently only about 23% of global greenhouse gas emissions are covered by a direct carbon pricing regime. Pricing levels globally average about $23 per ton of carbon dioxide equivalent, which are well below the minimum of $170 required to prevent the most harmful impacts of climate change. To reach complete coverage by 2030 with at least some level of carbon pricing, coverage will need to grow nearly three times the historical rate.

6) Eliminate Harmful Subsidies and Financing

Public and private investments continue to support activities that are incompatible with a sustainable future such as the development of new fossil fuel exploration and land degradation. Shifting investments toward a decarbonized future means stopping such harmful practices and redirecting capital to build a sustainable economy.

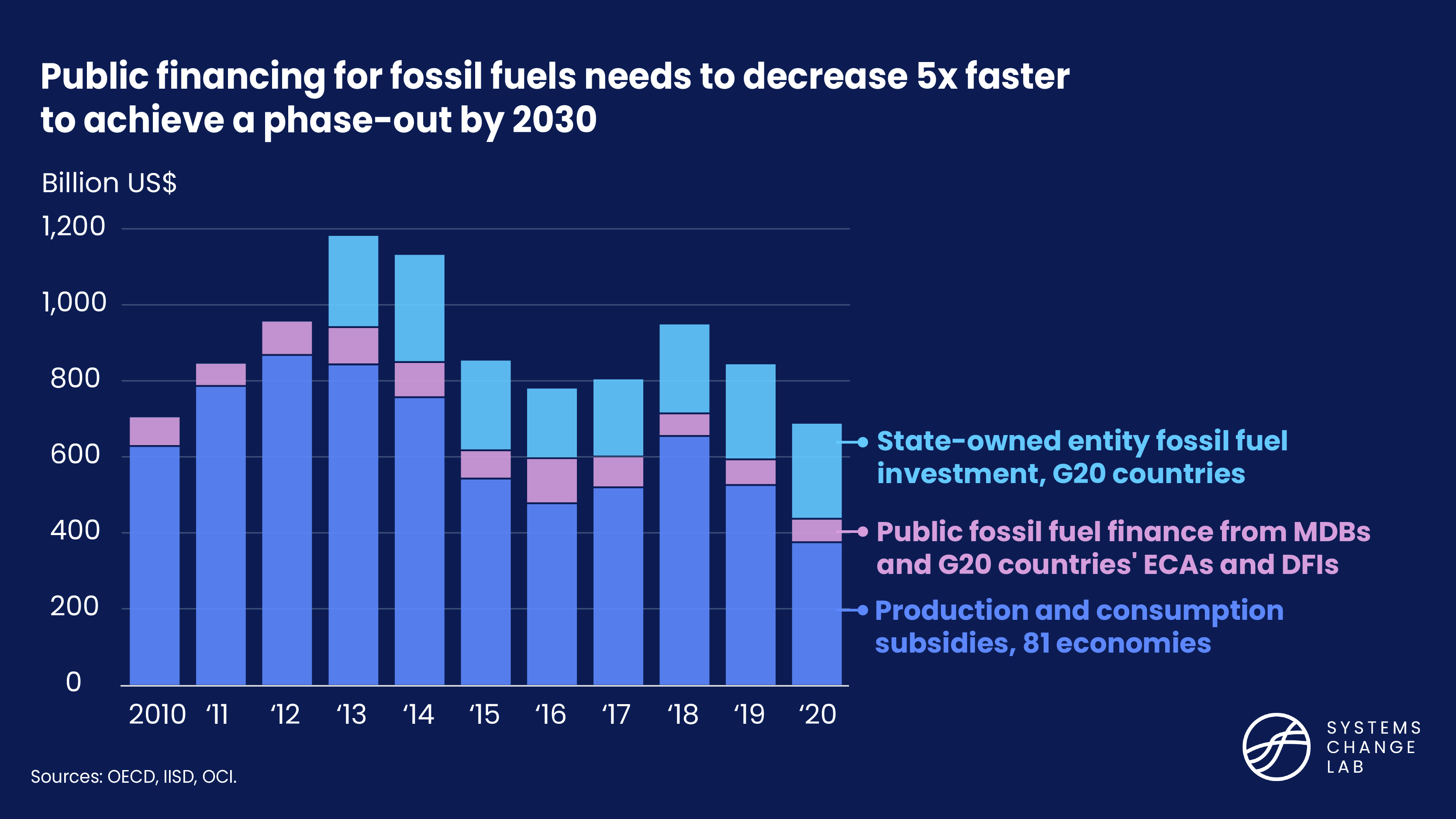

The public sector continues to provide significant financing and investment to the fossil fuel industry via subsidies, financing from development finance institutions and fossil fuel investments from state-owned companies. Public financing for fossil fuels totaled $687 billion in 2020 — still very far from the phaseout needed by 2030 which requires a decreased pace of almost five times the historical rate.

Similarly, governments persist in granting detrimental agricultural subsidies that incentivize the overuse of land and excessive use of fertilizers and pesticide, which contribute to environmental degradation. For example, total agricultural support reached $530 billion in 2021 for the countries in the Organization for Economic Co-operation and Development plus 11 major developing economies and it is estimated that 87% of such support is “price-distorting or harmful to nature and health.” Agricultural and fisheries subsidies should be structured to reduce their environmental harm and encourage sustainable practices.

Finance for a Sustainable Future

Across these six shifts, we have already seen some positive developments from both public and private finance in channeling financial flows toward creating a green and sustainable economy. Although these signs are encouraging, current levels of investment are still far behind what is required.

To ensure a livable, thriving planet, we must accelerate the positive momentum that has been built and scale up finance for climate and nature, wind down high-emitting assets and ensure that the prosperity brought by a sustainable economy will benefit underserved and marginalized groups. In this decisive decade, it’s time to act.